What we're reading about, 5/24/24

Climate, energy, and sustainability coverage we've been following around the web

(1) As we wrote about last week, CalPERS, the ~$486 billion California pension fund, has been publicly mulling a vote against the re-election of ExxonMobil’s CEO, Darren Woods, to the company’s board of directors, and possibly against re-electing other board members as well. This week, CalPERS confirmed they will vote against re-electing the oil and gas supermajor’s entire board.

The root cause of CalPERS’ discontent is ExxonMobil’s suit against two activist shareholders - Arjuna Capital and Follow This - who filed a shareholder resolution calling for the company to set ambitious “Scope 3” targets covering downstream emissions from the company’s products. Essentially, the proposal called for ExxonMobil to gradually exit the hydrocarbon business, which on a substantive basis, is a losing proposition with most investors - this is why a nearly identical proposal filed last year only won ~10.5 percent of the vote at the 2023 annual meeting.

A lot of the coverage of the ExxonMobil / Arjuna spat - which is moving forward in court, although ExxonMobil dropped Follow This, a Dutch activist group, from the suit - confuses the substantive merits of the proposal and the actual, quite technical issue at play, which is about both (i) the circumstances under which a company should be allowed to exclude a shareholder proposal from its proxy statement and (ii) how that standard should be enforced. This is because the SEC’s rule on shareholder proposals is extremely clear - the Arjuna / Follow This proposal was previously put forward twice in the last five years, and did not reach a critical 15 percent threshold of support when it was last submitted. If ExxonMobil had just sought permission to omit the proposal form the SEC, they would have gotten it.

ExxonMobil’s suit is much weirder than a substantive fight about the future direction of the business - it’s a very technical effort to change the mechanisms of US corporate governance. The proposal is seeking a “declaratory judgment that it may exclude Arjuna Capital and Follow This’s shareholder proposal from ExxonMobil’s proxy statement.” So the meta-level question is not whether the SEC’s rules on shareholder proposals apply, but whether the SEC alone can preemptively okay excluding a deficient proposal under the existing “no-action” process.

The tricky move that ExxonMobil is pulling is that instead of focusing on the resubmission criteria - where its case for excluding the proposal is black and white - its suit also invokes the ordinary business exception, which allows companies to exclude proposals that “[deal] with a matter relating to the company’s ordinary business operations.” The ExxonMobil complaint contains a lot of factual allegations - e.g., that Arjuna and Follow This “are not like most ExxonMobil investors,” holding ExxonMobil stock only to put forward shareholder proposals and not to make money - but these seem to be mostly beside the point. The key argument is that by directing the company’s approach to the energy transition, the Arjuna / Follow This proposal “seeks to usurp the role of management and the board” in determining company strategy:

(ExxonMobil Complaint, 1/21/24)

However, as the SEC’s lawyers articulated in Staff Legal Bulletin 14L, published in November 2021, there has long been a “significant social policy exception” to the ordinary business exception. This exception to the exception provides a path for proposals like the Arjuna / Follow This to be included on corporate proxy statements, and, ultimately, to be voted on by shareholders.

The problem with the ExxonMobil suit is that if it succeeds, it opens the door to any court with jurisdiction deciding willy-nilly how to interpret Rule 14a-8, which ultimately seems like a silly and inefficient way to govern the shareholder proposal process, relative to having SEC staff lawyers with many years of experience decide whether to grant no-action relief. It is also not clear whether such a regime would be practicable from a sheer organizational capacity perspective, given nearly all no-action requests are submitted in a narrow window in January and February. If the goal is to make application of the ordinary business exception more predictable, ExxonMobil’s legal strategy seems calculated to do the opposite of this.

Parenthetically, it is interesting to note that ExxonMobil did in fact seek no-action relief to exclude seven other activist shareholder proposals just this year, and succeeded (!) in four out of the seven cases - two of which hinged on the application of the ordinary business exception. This naturally leads one to question whether ExxonMobil is sincere in suggesting, via its actions, that district courts are a more reliable venue for interpreting and applying Rule 14a-8 than the existing procedure used by the SEC. If so, why rely on a district court to deal with one particular proposal under the ordinary business exception, and the SEC to deal with two others?

CalPERS’ public statement suggests that the stakes are about “silencing voices and upending the rules of shareholder democracy.” This is possible, though it begs the question of whether corporates will be able to successfully venue-shop for federal district courts that will interpret the ordinary business exception very broadly. What does seem certain is that this regime would create more confusion for corporates, activists, and ordinary investors to little end other than generating a lot of legal fees.

(2) Earlier this month, FERC adopted Order 1920, a new rule designed to overhaul long-range transmission planning by requiring companies that own and operate long-haul, high-voltage transmission lines to produce regional transmission plans with a twenty-year time horizon.

High-voltage line construction has slowed to a trickle in recent years, despite growing demand for electricity and an ever-growing “interconnection queue” of clean energy projects seeking to connect to the grid. The hope is that bringing greater transparency to the long-distance transmission planning process will ultimately drive transmission capacity expansion - removing a major long-term barrier to ramping up low-carbon electric generation. Per Grist, FERC is “essentially trying to prod the country’s many electricity providers to improve their planning processes and coordinate with each other in a way that encourages investment in this infrastructure.”

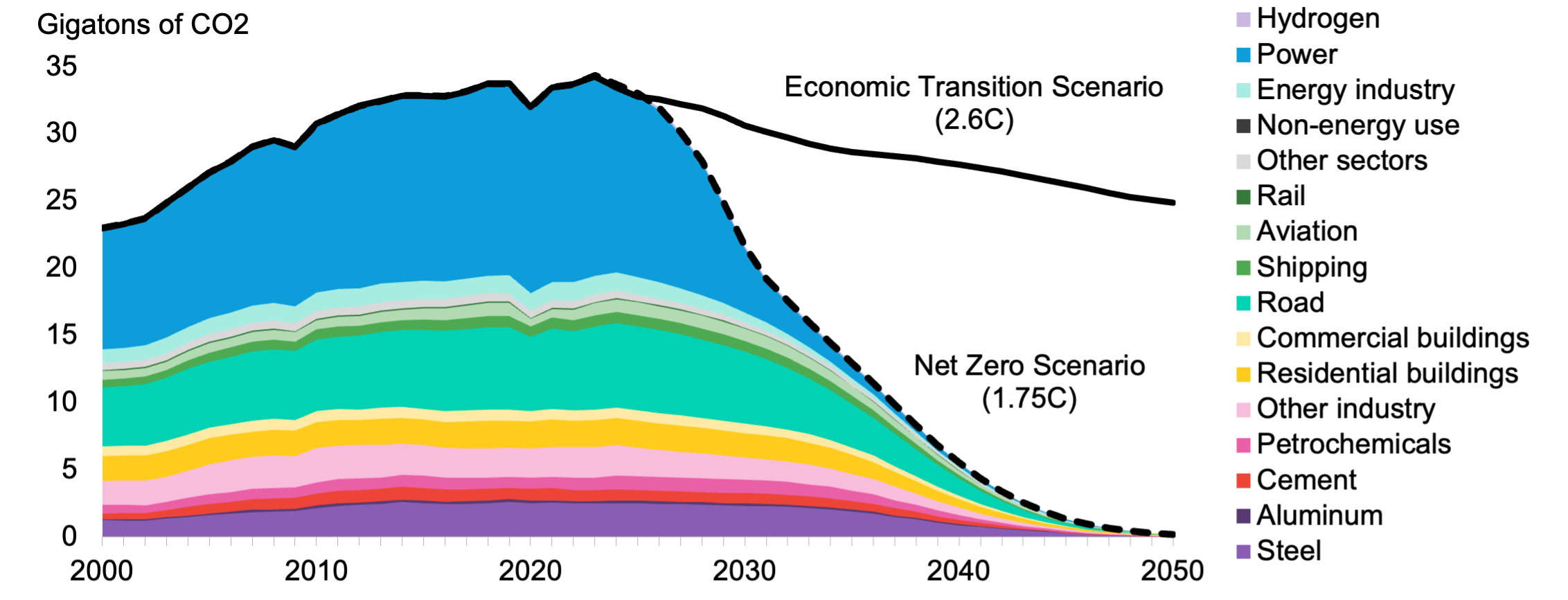

(3) BNEF is out with the latest edition of the New Energy Outlook, its flagship long-term energy modeling report. In its “Economic Transition Scenario” (ETS) - a base case anchored on current trends - warming reaches 2.6C above pre-industrial levels, while in the “Net Zero Scenario,” we manage to hold the line on warming of 1.75C. Notably, BNEF is projecting a 2023 emissions peak, with 2024E emissions down slightly (after rising 2.5 percent last year and 5.3 percent the year before, off of COVID-affected comps).

(BNEF)

The ETS scenario is, notably, is still a scenario, not a purely descriptive forecast. For example, it envisions consumption of all three major fossil fuels peaking in 2023 - much sooner than in base-case scenarios produced by national and international energy agencies, or (maybe obviously) by fossil fuel companies.

(BNEF)

Elsewhere: Oil & gas majors may have net-zero targets, but they aren’t aligned with a 1.5C scenario, according to think tank Oil Change; The fashion industry is a “carbon-accounting mess,” according to Bloomberg, which called out PVH for changing its emissions accounting methodology - producing an artificial 47 percent drop in emissions relative to the company’s base year.

|

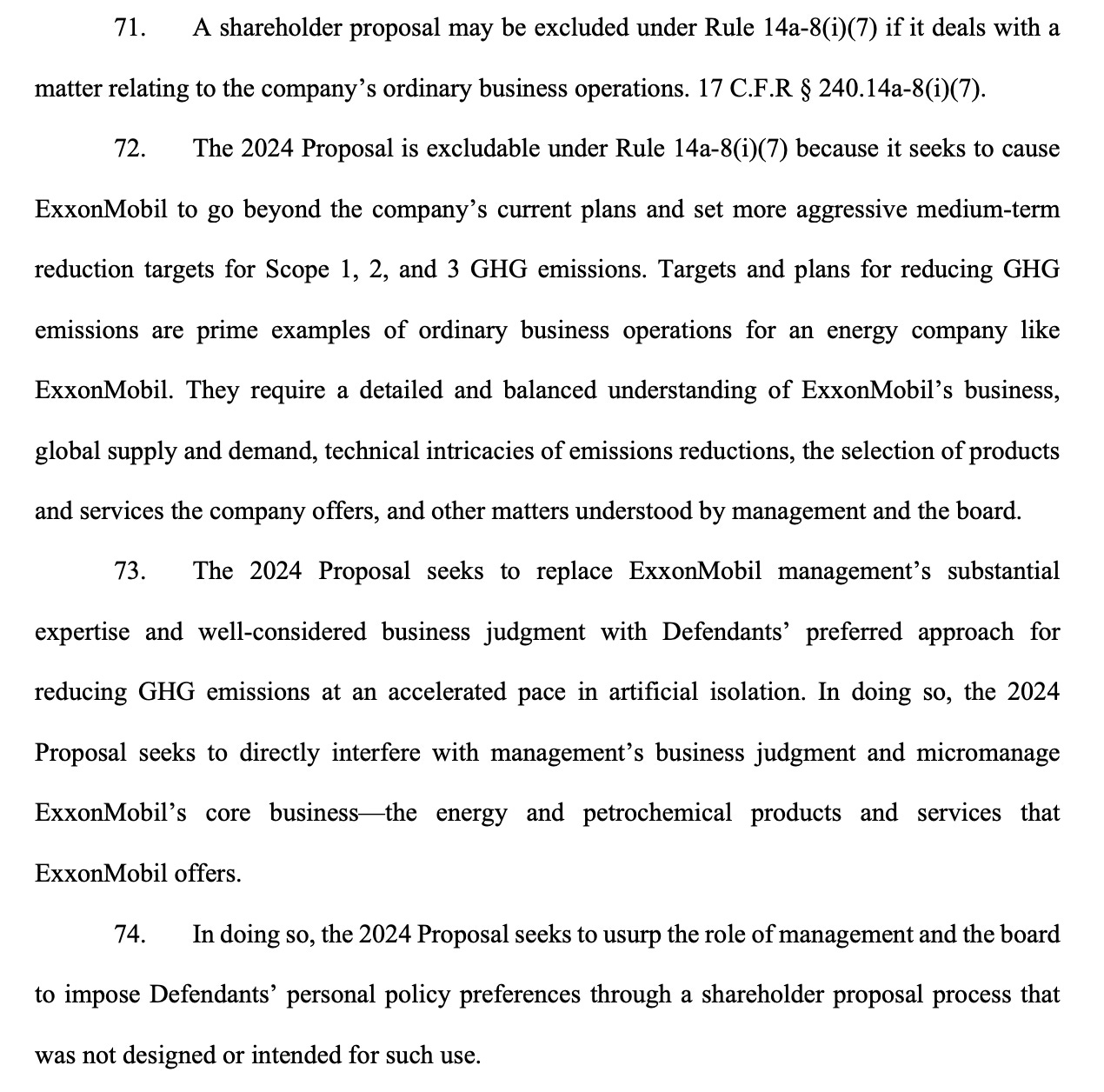

|