Going nuclear

Whither the "American nuclear renaissance"?

Note: This piece draws on the Jain Family Institute’s recent memo on reinvigorating the US nuclear industry. I was heavily involved in drafting the piece (especially the levelized-cost-of-energy modeling) but it was a team effort and we couldn’t have done it without the hard work of my colleagues, especially Jonah Allen and Sina Sinai.

At COP28 last December, twenty-one countries joined the US in a Declaration to Triple Nuclear Energy. The Declaration’s list of backers includes a number of countries with large and long-standing nuclear power industries, like the US, Canada, France, Japan, and the United Kingdom. Interestingly, it also includes a few countries where there are no nuclear power plants operating today, including developing countries like Ghana, Jamaica, and Morocco. But it is maybe most notable for the countries it leaves out - China, India, and Russia.

The electric generation capacity of all the reactors currently under construction in the world today is around 60 GW (compared to ~376 GW under operation, and assuming a ~5-8 year construction timeline, this implies ~2-3 percent annual capacity growth before taking plant closures into account). Over half of that pipeline (~34 GW) is being built in China, Russia, and India alone. The signatories of December’s declaration are home to only about a fifth of the global reactor pipeline. This mismatch stands out even more when you consider that the parties to the Declaration have over two-thirds of the world’s existing nuclear generation capacity.

(Statistical Review of World Energy)

In other words, the Declaration to Triple Nuclear Energy was made by countries that in recent years have not, in aggregate, been willing or able to grow electric generation from nuclear power, despite (mostly) being early adopters of the technology. Overall nuclear generation in these countries fell by roughly 8 percent between 2012 and 2022, while it grew by 39 percent in the rest of the world.

Parenthetically, it’s also interesting to look at the global division of labor in uranium production, fuel services, and reactor technology. The parties to the COP28 nuclear declaration produce a minority of the world’s uranium, and are home to a minority of the world’s enrichment capacity. While companies based in these countries, like Westinghouse and Framatome, have historically been global leaders in licensing reactor designs, only a few of the reactors under construction in China today use Western designs (representing ~25 percent of capacity under development).

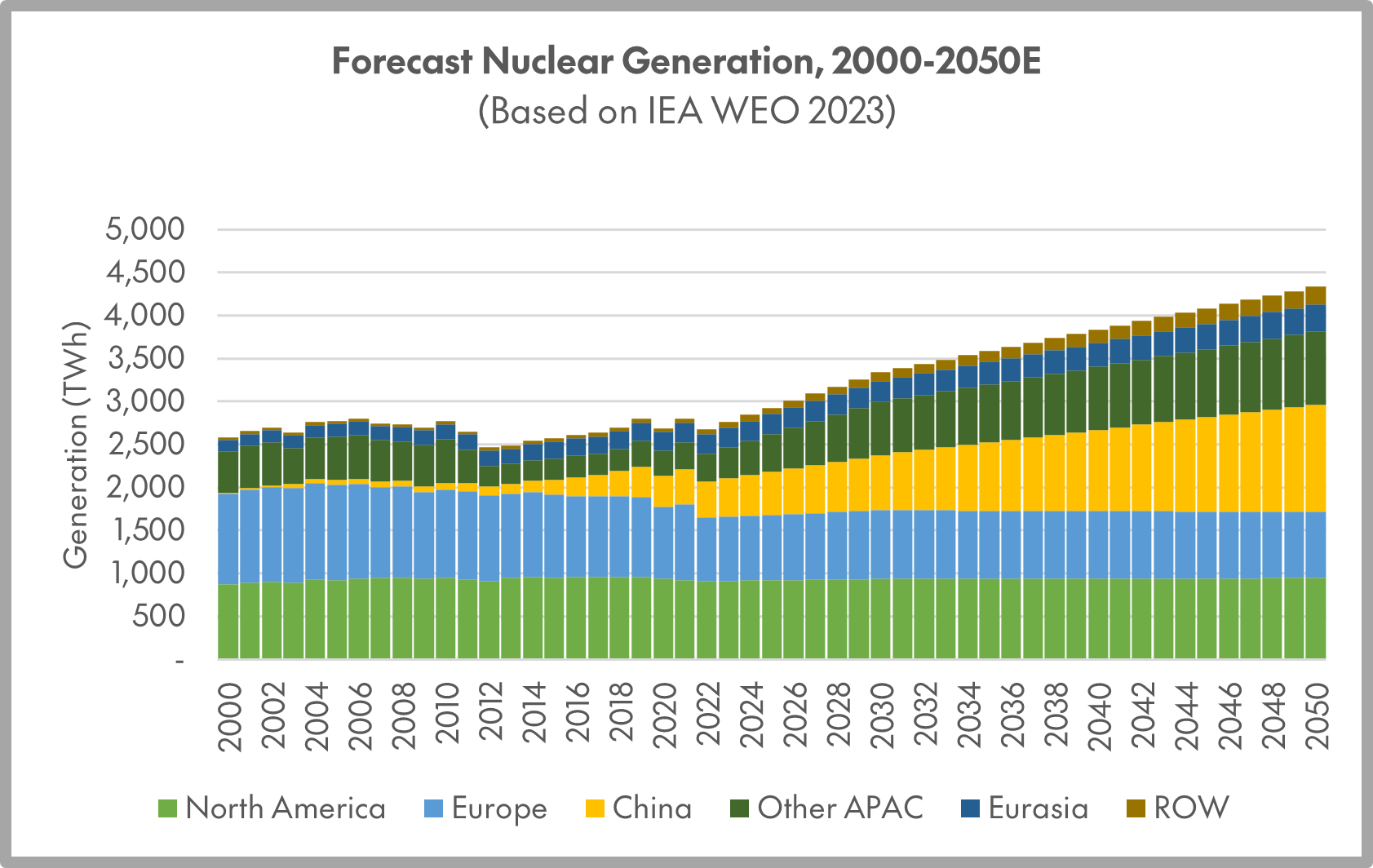

Before digging into why the countries behind the Declaration haven’t been building many nuclear plants, I think it’s important to note just how out-of-consensus this level of growth in nuclear generation would be. This is what the IEA’s Stated Policies Scenario (SPS) implies for the growth of nuclear power, by macro-region, over the next couple decades - 62 percent growth in generation by 2050, or a 1.7 percent annualized growth rate.

(IEA WEO 2023, Statistical Review of World Energy)

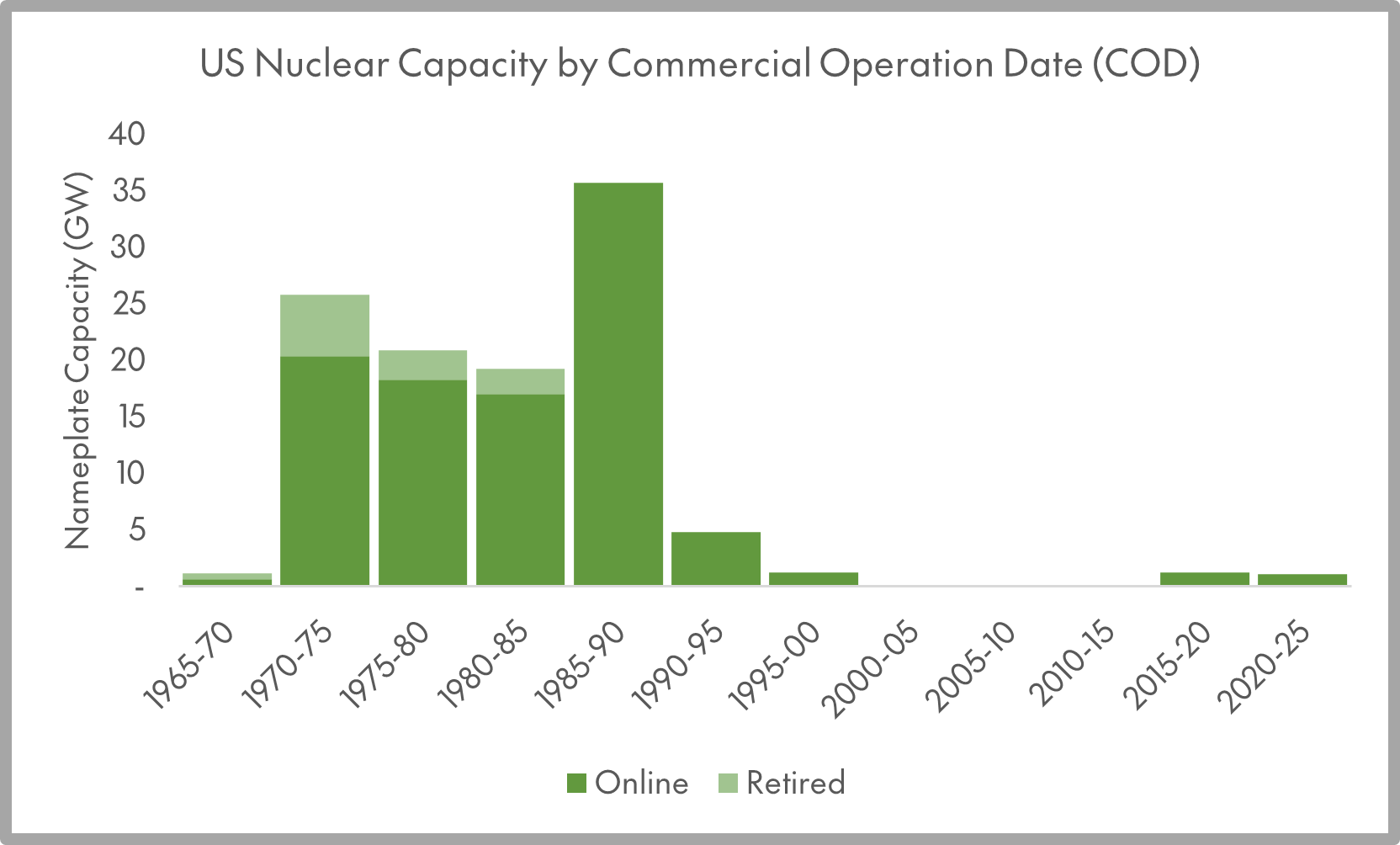

Even holding generation steady in the US, like the SPS assumes, will require significant investment to refurbish or replace existing plants. The US Nuclear Regulatory Commission (NRC) licenses plants to operate for 40 years; licenses can be extended in 20 year increments. 90 percent of US plants have already extended their licenses once, and further extensions are possible; but it seems hard to believe that the capacity of the US nuclear fleet will be able to tread water without at least some new construction starts.

(EIA Electric Generator Monthly)

Today, nuclear power is the second-largest source of low-carbon electricity globally, and one without the land-use / siting challenges of solar, wind, and hydropower. Whether the goalpost is “tripling” global generation (a self-avowedly “aspirational” goal), or just maintaining the current level of nuclear generation, we will need to figure out how to build nuclear plants in the US, Europe, and other developed markets again. Replacing ~2,700 TWh of nuclear with combined-cycle gas (via either greenfield projects or slower retirement of existing gas plants) would mean a ~1.28 Gt increase in emissions.1

The economic challenge of building more nuclear plants in, let’s say, the member countries of the OECD, boils down to two facially simple problems. One, all recent US and European reactor projects have been hugely behind schedule and over budget. Two, it’s been very hard to keep existing reactors financially viable in certain market contexts - thinking mainly here of restructured markets in the US.

(Vogtle Construction Monitor’s Report, EDF, Press Reports)

What I find interesting about the construction cost issue is the way it implicates our mental models for thinking about technology. Because there is no real a priori way to tell which technologies will experience “learning effects” over time, we tend to give lab- and demonstration-scale technologies the benefit of the doubt. The assumption that new energy technologies will see 18-to-20 percent cost reductions with each doubling in cumulative capacity is a widespread rule of thumb - it pops up everywhere in energy forecasting, for example, in the assumptions that power the US EIA’s Annual Energy Outlook.

(EIA)

On the other hand, cost projections for future nuclear generators anchor on the sorry record of recent Western projects. See, for example, this recent New York Times op-ed by Stephanie Cooke on the “fantasy of reviving nuclear energy”:

The Energy Department estimates the total cost of such an effort in the United States at roughly $700 billion. But David Schlissel, a director at the Institute for Energy Economics and Financial Analysis, has calculated that the two new reactors at the Vogtle plant in Georgia — the only new reactors built in the United States in a generation — on average, cost $21.2 billion per gigawatt in today’s dollars. Using that figure as a yardstick, the cost of building 200 gigawatts of new capacity would be far higher: at least $4 trillion, or $6 trillion if you count the additional cost of replacing existing reactors as they age out.

(New York Times)

This is obviously a punitive calculation - adding 200 GW of new nuclear capacity in the United States between now and 2050, let alone 300 GW, would imply adding ~7 GW per year, a pace reminiscent of the US nuclear industry’s growth in the 1970s, or, indeed, China’s current reactor construction campaign. It is very hard to accept the proposition that building that many reactors at that kind of pace would not result in learning effects, particularly in the project management and “soft costs” that drive much of the cost variance between the Vogtle project and recent builds in South Korea, China, and the United Arab Emirates.

But what’s interesting is less the specifics of the op-ed’s argument, and more the way that the conversation on nuclear gets stuck on this point, because Vogtle (one of the most expensive nuclear projects ever) has become the only point of reference for what a greenfield nuclear project in the US looks like. Nuclear ends up getting categorized as a technology that had it’s chance, and failed, while carbon management, low-emissions hydrogen, and long-duration energy storage supposedly need only a gentle push to start making their way down the experience curve.

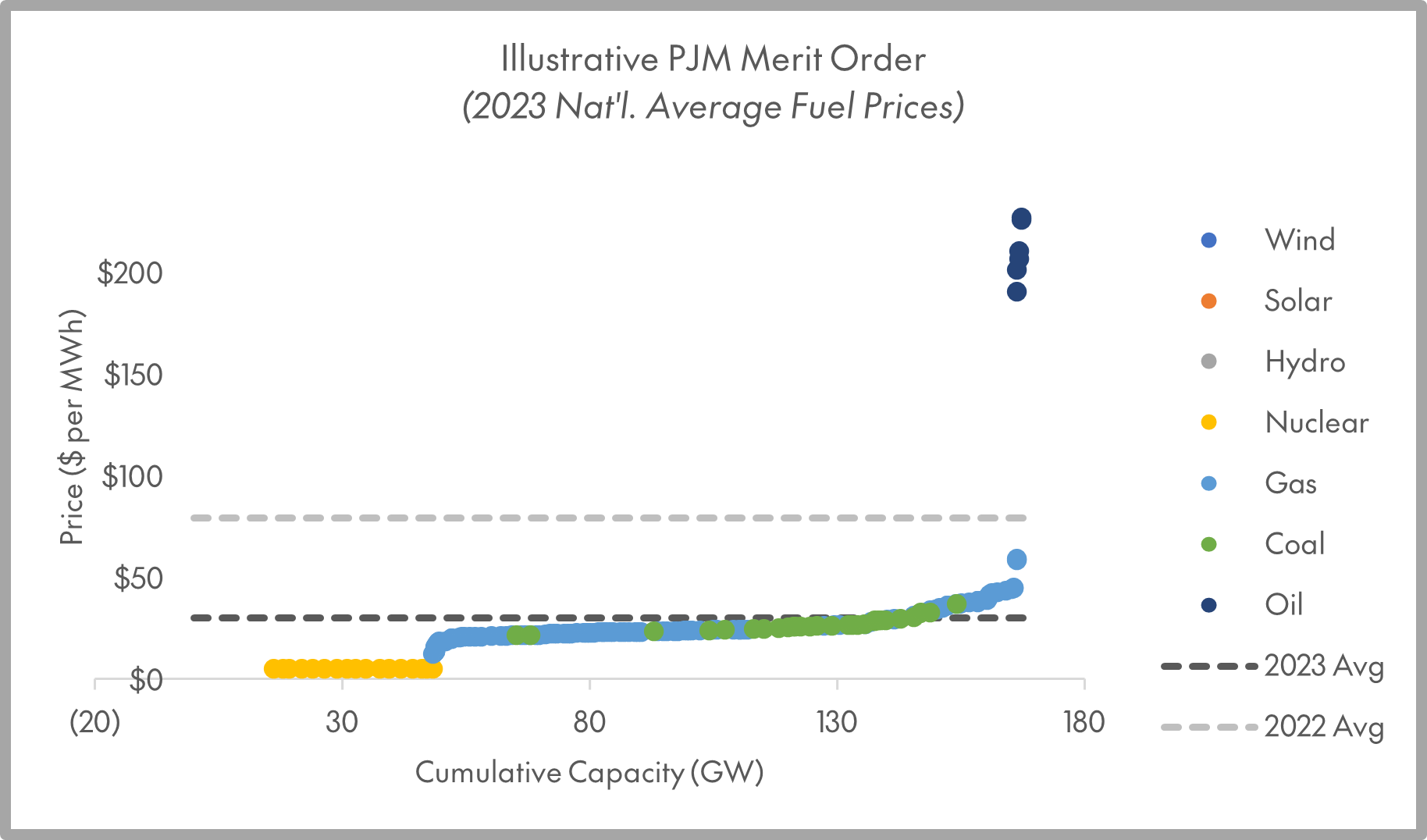

The other challenge for the US nuclear industry is keeping existing plants economically viable. The key concept here is the merit curve - essentially, the short-run supply curve for electricity. In a (stylized) restructured electricity market, power plants bid to offer power at their marginal cost. The clearing price of power for a given quarter- or half-hour time slot is the cost of the last MWh needed to meet demand (“load”).

Nuclear fuel is relatively cheap, even at today’s high uranium, enrichment, and conversion prices - something like $5 to 7 per MWh of electricity - while fuel is the biggest component of the cost of power from fossil fuels, running from the $20 to 30 per MWh range for the most efficient plants (combined-cycle gas plants used for baseload) to $40 or more per MWh (more sparingly used gas plants). The hourly average load in the territory served by PJM, a US independent system operator (ISO) in 2023 was ~92 GWh (including exports). Our illustrative supply curve (which cheats a little bit by using national-average costs for fossil fuels) predicts a ~$25 per MWh price of power at that level (the actual hourly average locational marginal price, or LMP, in PJM was $31 per MWh last year). Peak load for the ISO was much higher, at 153 GWh. Our simple model predicts a price of about ~$50 per MWh at that level of load.

In reality, realized prices will turn out higher than in this simple exercise, because variable renewables - solar and wind - only generate power when the sun is shining or the wind is blowing, not in response to demand. So at any given point in time, the market needs to source power from further out on the supply curve than if solar and wind were available 24/7. Said differently, there is about 13 GW of solar and wind generation capacity in PJM. If all of this capacity were unavailable at the average hourly load of 92 GWh, it would increase prices by 3 percent. If it were unavailable at the peak load of 153 GWh, it would increase prices by at least 59 percent.

(Author’s calculations based on EIA data)

What all this means is that the economics of nuclear power are amenable for use as a baseload power source over the short run. Burning the marginal ton of fuel is always going to generate a positive contribution profit for the operator, because the price of power (most of the time) is set by combined-cycle gas plants, with a marginal cost in the mid-to-high $20s per MWh, versus a fuel cost of $5 to 7 per MWh for nuclear. The trouble begins when we consider the operating and maintenance (O&M) costs faced by nuclear plants, which are substantial - $17, on average in the US, which means nuclear has the highest average O&M costs of any widely used generation technology. This means that the US nuclear fleet was, on average, losing money for every MWh of power until fossil fuel prices started spiking in 2021/2022.

Obviously, this was not such a big problem for traditionally regulated utilities, able to recoup the costs of their overall asset base through rates levied on all customers. But it made for a very difficult operating environment for competitive nuclear plants in restructured markets - which were heavily over-represented in US nuclear plant closures over the course of the 2010s.

(BNEF)

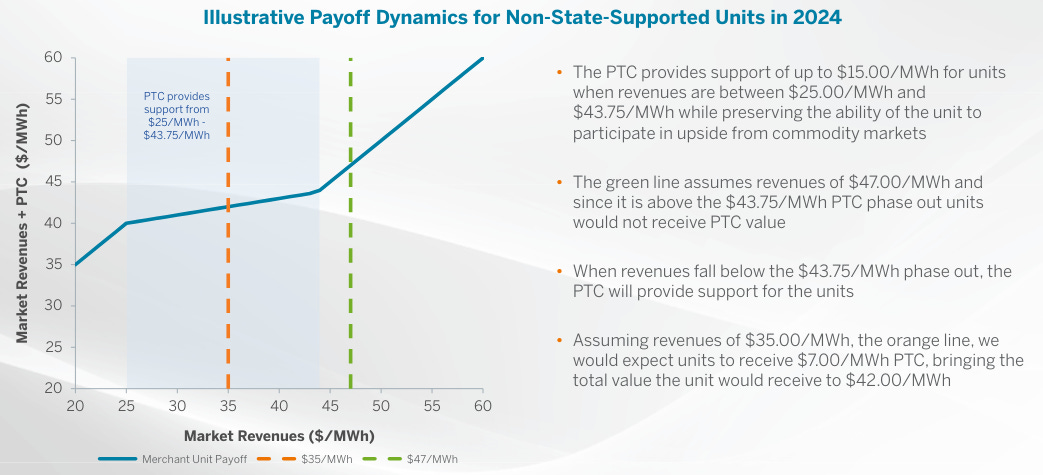

The Inflation Reduction Act (IRA) has already gone a long way toward fixing this problem with the new tax credit for existing nuclear plants (45U). Constellation Energy, the largest owner of competitive nuclear plants in the country, has some nice slides in its “Nuclear 101” deck explaining the dynamics of the credit:

(Constellation Energy)

The street seems to appreciate the way 45U (and the shift to an environment with growing demand for electricity) has changed the outlook for existing nuclear assets. Constellation’s stock price is up 148 percent since it began regular-way trading after its spinoff from Exelon. But it remains to be seen whether investor curiosity about the space will translate to shovels in the ground. One fascinating story to watch over the next few years is Holtec International’s effort to refurbish and restart nuclear generation at Michigan’s shuttered Palisades nuclear plant (operated from 1971 to 2022) with the help of a $1.5 billion loan from the DOE. Brownfield projects like this could be an interesting way to backfill plant closures without banking on cost reductions for future greenfield plants.

In his (excellent) energy paper from earlier this year, JPMorgan’s Mike Cembalest essentially argues that the (much lower) cost of reactor construction in other parts of the world is totally incomparable to US and European builds:

Average completion times [for nuclear reactor projects] in developed countries ranged from 4 to 10 years for plants whose construction began from 1960 to 1990, but there are so few observations for developed countries since 1990, it’s impossible to know. Plants have been completed in 6-8 years in developing countries such as China, India and Russia but this has nothing to do with what can be accomplished in the West.

(JPMorgan)

In the nuclear memo I penned with my JFI colleagues, we dig into the literature on costs, and benchmark a US AP1000 reactor (Vogtle) against the KEPCO APR1400 (using the UAE’s Barakah plant as an example). I think there is some indicative evidence that Cembalest could be wrong, and that there are portable lessons for the US from reactor construction campaigns overseas. But, at a prospective cost of ~$17 billion for a new two-reactor plant, it will take a little more conviction than that (and a lot of capital) to put the proposition to the test.

Based on NREL’s collection of literature estimates of the lifecycle emissions factor for nuclear (pressurized water reactors) versus a combined-cycle plant using shale gas.