What we're reading about, 2/23/24

Climate, energy, and sustainability coverage we've been following around the web

(1) Researchers from the University of Nevada and University of Michigan published a paper in the journal Energy Research & Social Science digging into corporate emissions data from the Carbon Disclosure Project (CDP).

By looking at facility-level emissions, they were able to tease out the impact of corporate net-zero initiatives from the effects of state and local policy incentives:

“...we disaggregate CDP corporate GHG disclosures down to the facility level, enabling us to assess the factors driving corporate decarbonization with greater precision than is possible at the level of aggregate firm emissions. Thus far, the aggregate has been the predominant scale of analysis in research on corporate climate efforts. This is the first study to disaggregate corporate emissions from CDP disclosures down to the facility level in order to analyze the respective roles of corporate initiatives and subnational policies in driving decarbonization.”

The authors found that corporate initiatives alone had little impact on emissions trends compared to state-level energy efficiency incentives:

(2) Electric generation from coal-fired plants in Europe fell by 26 percent last year, and gas generation fell by 15 percent, driving a record decline in power sector emissions, according to energy consultancy Ember’s European Electricity Review 2024, out earlier this month.

(Ember)

Solar generation grew by 36 TWh (versus 48 TWh in 2022), while wind power grew by 54 TWh (versus 33 TWh in 2022). All in, renewable power in Europe saw its biggest year of growth ever. Combined, wind and solar comprised a 27 percent share of total power generation, almost overtaking coal and gas at 29 percent. The European power sector will need to nearly double the current share of renewable generation to keep up with the EU’s Renewable Energy Directive, which requires all member states to derive at least 42.5 percent of their power (!) from renewables by 2030.

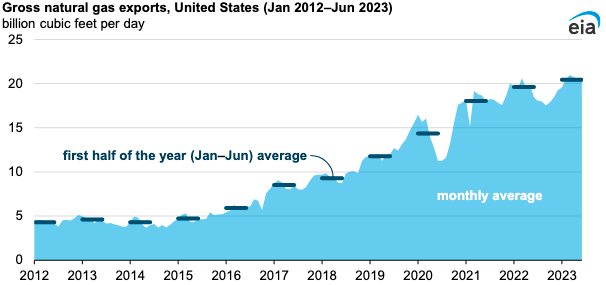

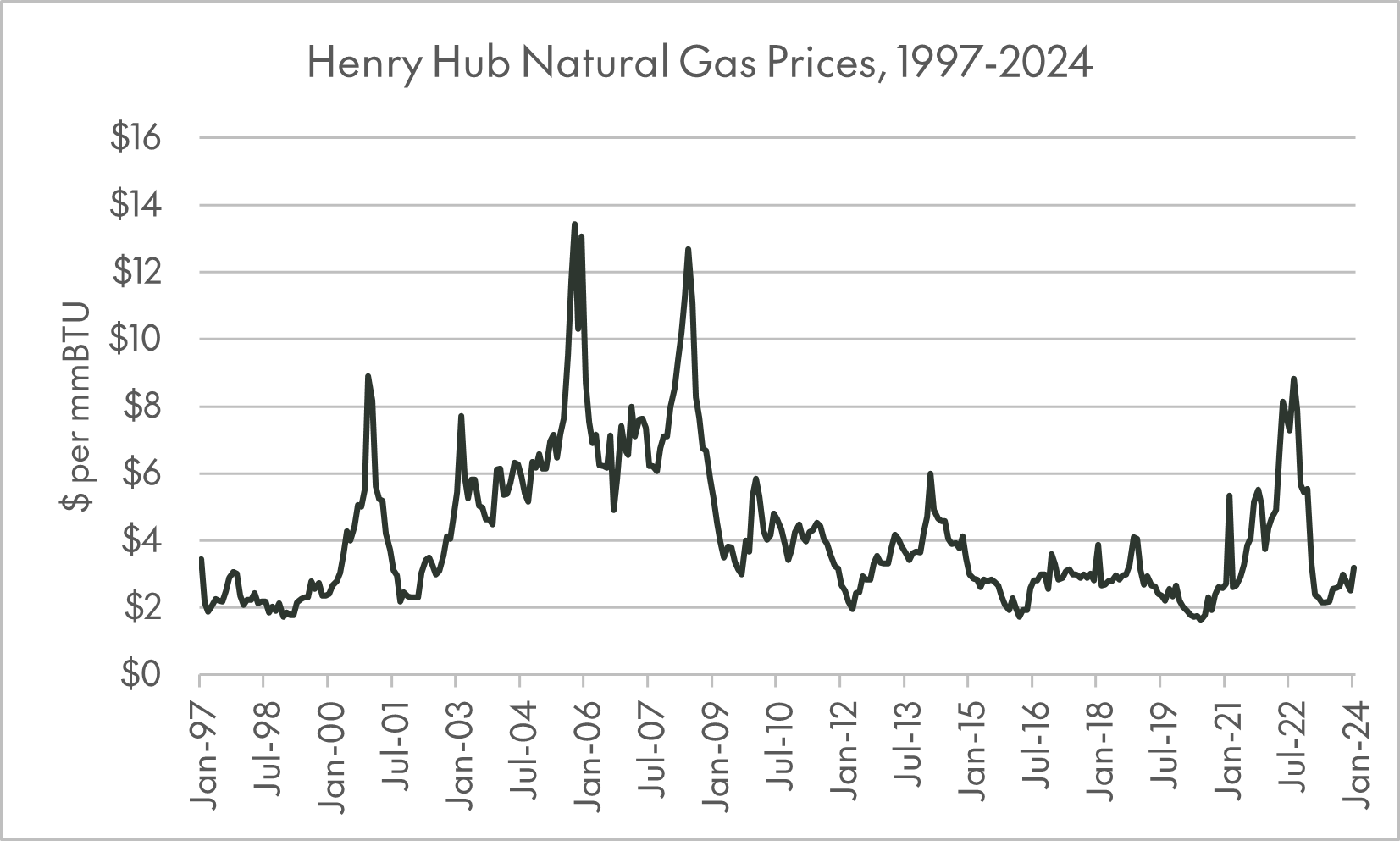

(3) Canary Media’s Julian Spector dug into some of the current debates on expanding US liquefied natural gas (LNG) export capacity - (i) whether it will enable Europe to transition away from Russian gas, (ii) whether it will increase domestic energy prices, and (iii) whether it will have a positive or negative impact on global emissions.

Ironically, LNG access may be a less urgent issue for Europe than it seemed to be even a year or two ago, thanks to record-breaking increases in renewable generation. And it’s not necessarily the case that higher LNG export capacity means more expensive natural gas stateside; natural gas exports have never been higher, but because production has been so strong, domestic natural gas prices are actually crashing.

(EIA)

(4) Heatmap’s Robinson Meyer laid out a cheat sheet explaining the different regulatory changes being mooted in the US that fall under the umbrella label “permitting reform.” Broadly speaking, it’s more difficult to build new renewable projects, power lines, and the like than it needs to be if we’re going to decarbonize.

One index of this problem is the size of the interconnection queue - the roster of proposed projects waiting for permission to connect to the grid - which is growing exponentially:

(LBNL)

(5) The New York State Common Retirement Fund – one of the largest public pension funds in the US – will restrict its investments in eight oil and gas companies and divest a small share of its holdings in ExxonMobil (XOM). Per Reuters, the move follows “a review of the companies' readiness to transition to a low-carbon economy.”

The fund had an estimated value of $254.1bn at the end of the last fiscal year (ending June 30, 2023). Out of that total, just $26.8mn in corporate bonds and actively managed equity funds will be impacted by the new policy, nearly all of which ($25mn) is XOM stock.

The partial divestment from XOM is partly a result of XOM’s lack of Scope 3 emissions reduction targets relative to its peers like Chevron (CVX), BP and Shell (SHEL). The retirement fund will still hold approximately ~$500mn in XOM shares across its passive funds and other holdings.

(6) Despite all the noise about the political polarization of ESG, BlackRock has steadily posted net ESG inflows every quarter for the past two years. According to data provided by Morningstar Direct to Bloomberg, BlackRock’s ESG-related assets under management grew 53% from the beginning of 2022 through the end of 2023 to ~$320bn in ESG-related assets under management.

At first glance, that growth is even more impressive when you consider that the S&P Global Clean Energy Index fell 20 percent in 2023. But it makes sense when you realize that investing in clean energy has little to do with what BlackRock means by “ESG.”

Many of BlackRock’s ESG funds are passive, and track ESG indices from third parties. The BlackRock ESG fund that saw the biggest inflows, the the iShares Climate Conscious & Transition MSCI USA ETF (USCL) tracks an index from MSCI called the “MSCI USA Extended Climate Action Index,” which employs the following methodology:

The MSCI USA Extended Climate Action Index is designed to represent the performance of companies that have been assessed to lead their sector peers in terms of their positioning and actions relative to a climate transition. MSCI Extended Climate Action Indexes use MSCI ESG Business Involvement Screening Research and MSCI Climate Change Metrics to identify companies that are involved in the following business activities such as Controversial Weapons, Tobacco, Thermal Coal Mining, Oil Sands, Nuclear Weapons and Producers of Civilian Firearms.

(MSCI)

Conversely, the ACS US ESG Insights Equity Fund follows a vanilla US-stock benchmark, albeit not a very widely used one (the FTSE USA Index), and seems to apply a proprietary ESG approach developed by BlackRock. From the BlackRock website:

The aim of the Fund is to provide exposure to a portfolio of companies within the FTSE USA Index (Index) that is managed, using environmental, social and governance (ESG) related exclusionary screens and a proprietary ESG framework of the Investment Manager (IM), to 1) have a reduced exposure to certain business activities for ESG related reasons, 2) have a higher weighted average exposure (relative to the Index) to companies that score more highly on certain ESG criteria, 3) reduce its overall carbon emission intensity over time, and d) have a higher percentage (relative to the Index) of its revenues classified as green revenues (each as further described below). It aims to achieve these ESG related aims whilst also balancing the return and risk profiles of the Fund to be broadly similar to the Index.

How could you even tell how these funds differ on “ESG-ness”? Skimming their top holdings, the difference between them seems to be that USCL owns more Microsoft and less Nvidia. We would be hard pressed to explain what that has to do with climate change (or “ESG”).

Further Reading

Does LNG really fight climate change? 5 common LNG claims, examined (Canary Media)

European Electricity Review 2024 (Ember)

Chart: Wind and solar are closing in on fossil fuels in the EU (Canary Media)

New York pension fund to divest some Exxon holdings (Reuters)

BlackRock’s ESG Fund Business Is Soaring Despite Attacks by the GOP (Bloomberg)

|

|