Regulated value creation (pt. 1)

Decarbonizing power means thinking like a utility

Getting to net zero by 2050 will require getting to net zero in the electric power sector much sooner. All of the low-carbon technologies that are being deployed at scale today either allow us to produce cleaner electricity (solar, wind, etc.) or to substitute electricity from the grid for fossil fuels - think ICE cars to EVs, boilers to heat pumps, and coke-fueled blast furnaces to electric arc furnaces for steelmaking. The result is the framework that JP Morgan’s Michael Cembalest recently called Electravision: produce the cleanest electricity possible, and use electricity to serve as much of the world’s energy needs as possible.

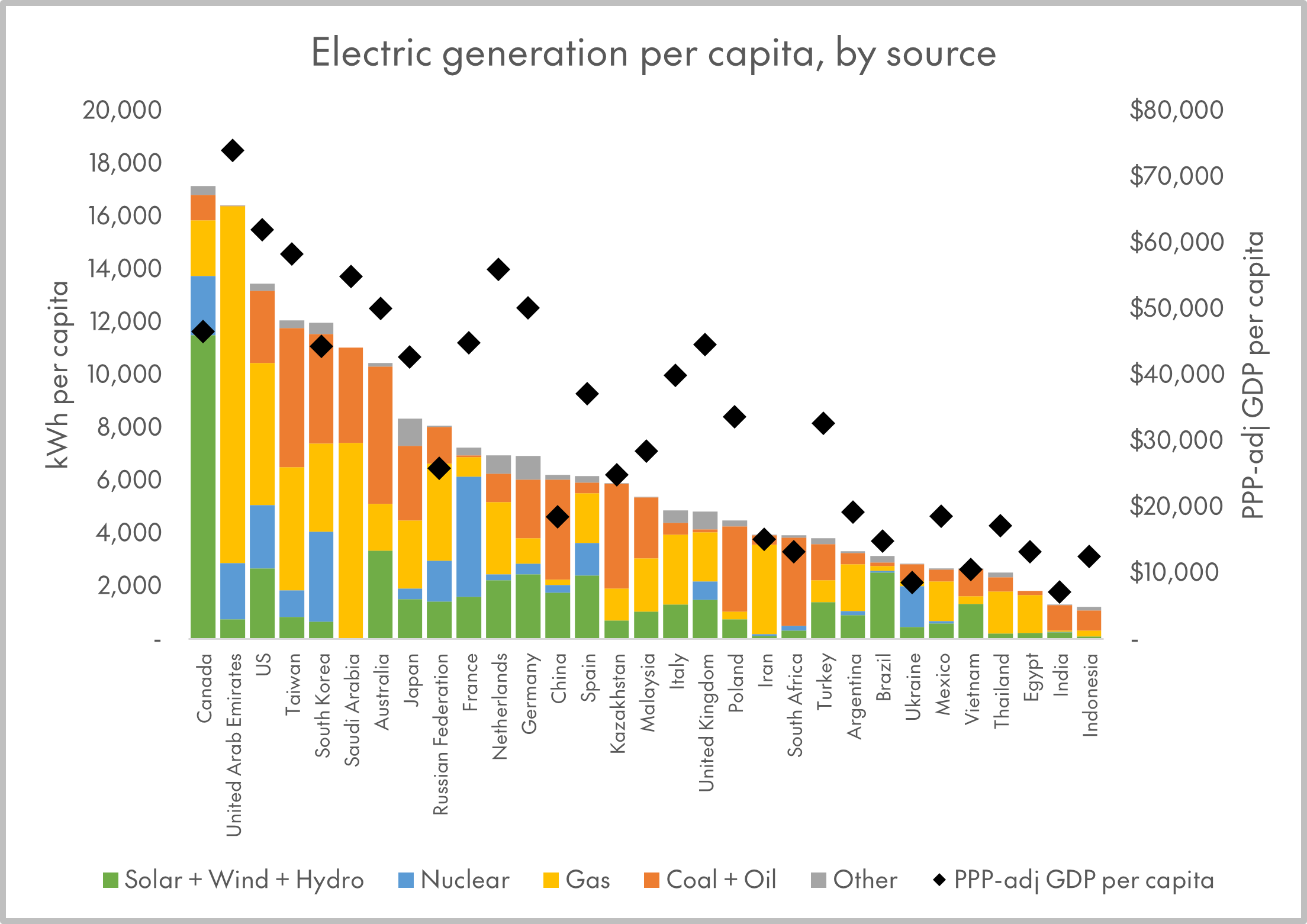

Figs. 1-2: Electricity generation is highly correlated with PPP-adjusted GDP. Note the impact of natural endowments, reflected in the high share of hydroelectricity in Canada and Brazil, and hydrocarbons in the UAE and Saudi Arabia, which generates ten times as much electricity from oil, per capita, as any other large country.

(Statistical Review of World Energy)

In the US, the Biden administration has set a goal for 100 percent “carbon pollution-free” electric generation by 2035 (this includes fossil fuels with carbon capture and storage, or “CCS”). The White House published the Long-Term Strategy of the United States (LTS) in November 2021, to deliver on the Paris Agreement’s expectation that signatories “strive to formulate and communicate long-term low greenhouse gas emission development strategies.” In the LTS, electric generation from unabated coal and gas falls quickly by the end of the decade. However, the share of transportation-related energy coming from oil and energy for industry coming from gas remains stubbornly high into the 2030s.

Fig. 3: LTS projections for US electric generation by technology under the “Balanced Advanced” (left) and “Lower Power” (right) scenarios.

(Joule)

This means that, in the make-or-break phase of the energy transition, the market structure and regulatory setting of the utility industry will be all-important - not just in determining how fast we decarbonize electric power, but how we do it. That includes not just which technologies win out (variable renewables, batteries, long-duration energy storage, power-to-fuel cycles…), but also the distributional question of how the costs and benefits of the energy transition will be allocated between utility shareholders, workers, ratepayers, and different levels of government.

In this piece - the first of several focused on the US utility industry - I’ll (i) lay out the distinction between different electric utility business models, and (ii) highlight some benchmarking work my team did on the generation mix and emissions intensity of the fifty largest vertically integrated utilities (at the OpCo level) in the US. In subsequent pieces, I’ll introduce a simple model of how utilities create value, illustrated by the best-of-breed US utility, Florida Power & Light Co., and touch on how utilities’ net zero aspirations could flow through to their credit and equity stories.

I. Electric market deregulation and the great unbundling

In the 1980s and 1990s, electricity markets in the United States (and around the world) were restructured. Historically, monopoly utilities, mostly regulated at the state level1 owned generation, high-voltage transmission, and lower-voltage distribution assets. Rapidly growing electricity demand, spurred on by the adoption of air conditioning and home appliances, combined with economies of scale at coal-fired steam plants, meant utilities could reliably grow earnings while keeping retail electricity prices down.2

Under traditional utility regulation, regulators define a target return on equity and capital structure (equity-to-total-assets ratio) for utilities. Utilities decide whether to invest in new power plants and transmission lines, and then set rates for different classes of customers (residential, commercial, and industrial users of power) in order to recover their costs. Thus, “ratemaking” ends up being a tightly coupled, public-private planning process, in which regulatory feedback (which in theory reflects the “voice of the consumer”) loops back into the utility’s investment decisions.

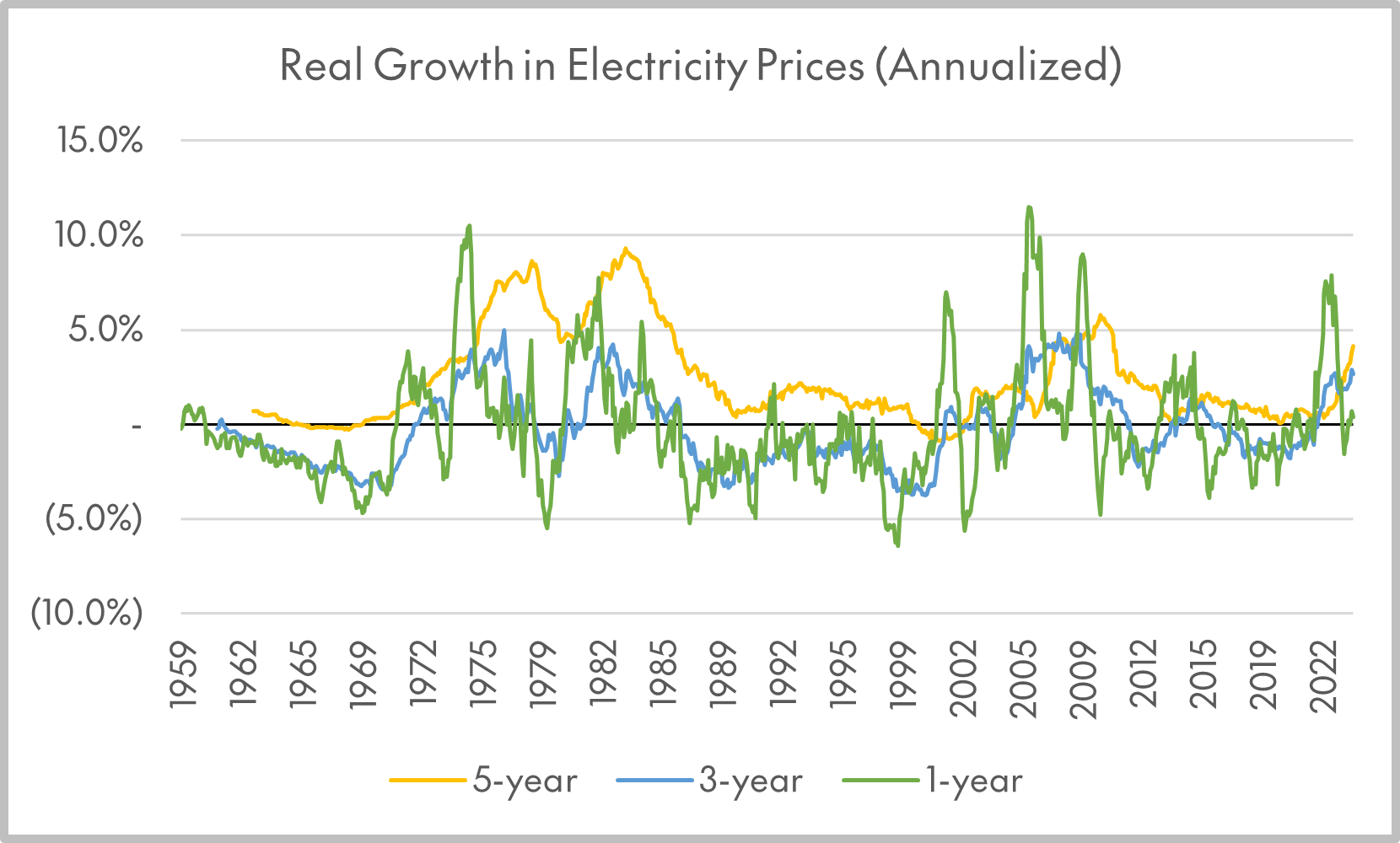

Fig. 4: “Real” growth in electricity prices is approximated here by the difference between growth in the electricity component of CPI and that of the overall consumption basket. PPI data shows the same trend - periods of electricity price deflation in the 1950s-60s, mid-80s to late-90s, and 2010s, and electricity price inflation from the 1970s to early 1980s and again in the 2000s. The recent uptick in electricity prices is suggestive.

(FRED)

Many factors converged to promote restructuring as the solution to the period of increasing real electricity prices that began in the 1970s. Landing on a unified explanation for the why and how of restructuring is beyond the scope of this piece, but a few themes stand out:

The Public Utilities Regulatory Policies Act of 1978 (PURPA) forced utilities to purchase power from “qualifying facilities,” typically small renewable and cogeneration plants, at “avoided cost,” sometimes calculated very generously. PURPA promoted the growth of an independent, investor-owned generator industry and also saddled many regulated utilities with expensive, long-term power purchase agreements (PPAs).

Construction costs and project timelines for nuclear power plants were already ballooning by the late 1970s. Globally, nuclear plant grid connections peaked in 1985, but construction starts actually peaked as early as 1975. In the US, many projects were cancelled and regulators pushed back when utilities tried to recover stranded costs through higher rates, leading to poor returns for utility shareholders, and, in some cases, bankruptcies.

Improving gas turbine technology weakened economies of scale in generation, because gas turbines could be operated at a comparable cost to traditional, steam-based power plants at much smaller scales. This made self-generation by industrial customers a viable threat.

Intellectually, the electric grid came to be seen as a “network industry” with analogies to telecommunications and transportation. Free-market oriented economists argued that high-voltage lines could be treated as common carriers, even if local distribution was a natural monopoly. It became common sense in policy and academic circles that a competitive generation sector would lead to lower costs.

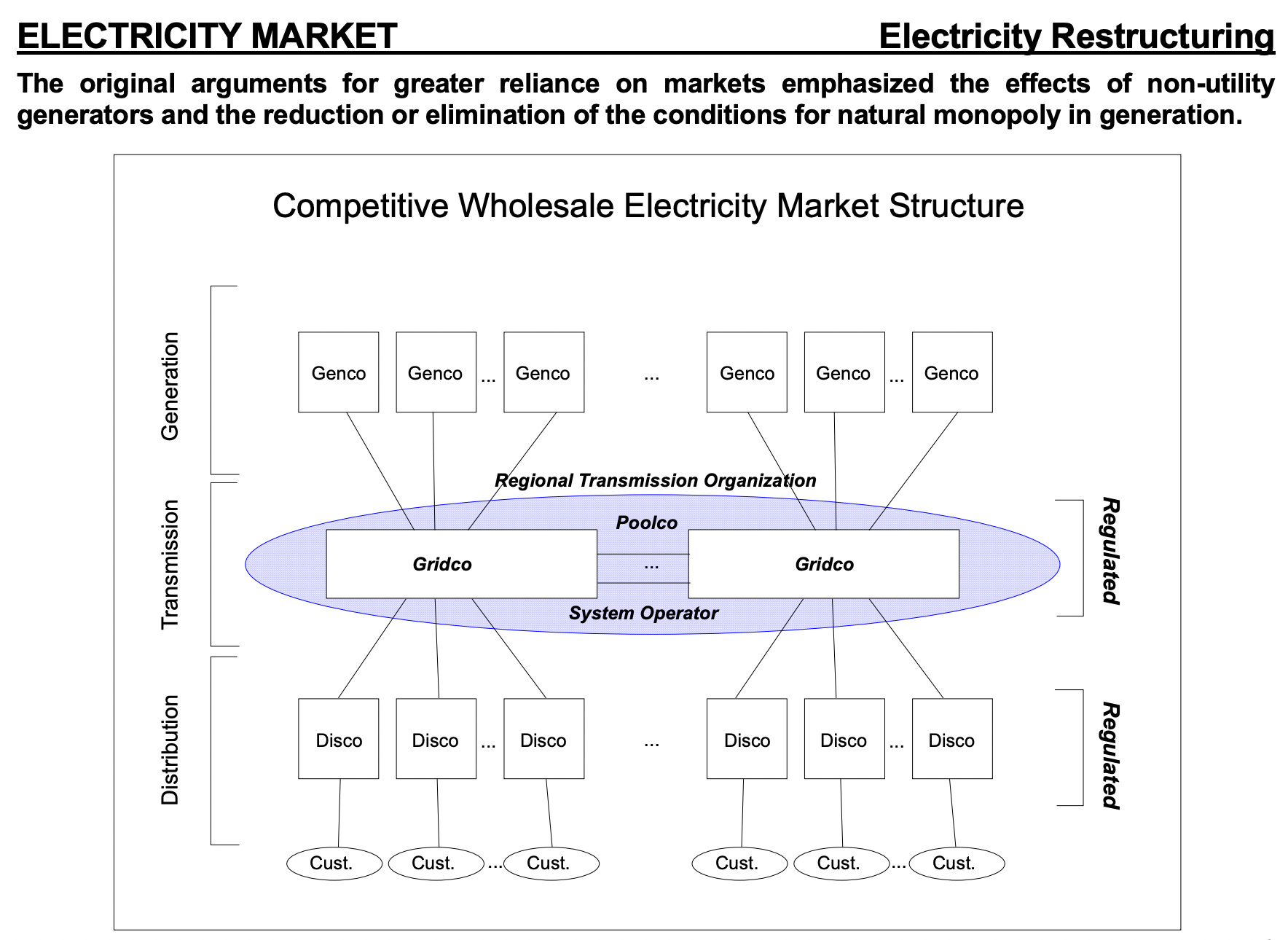

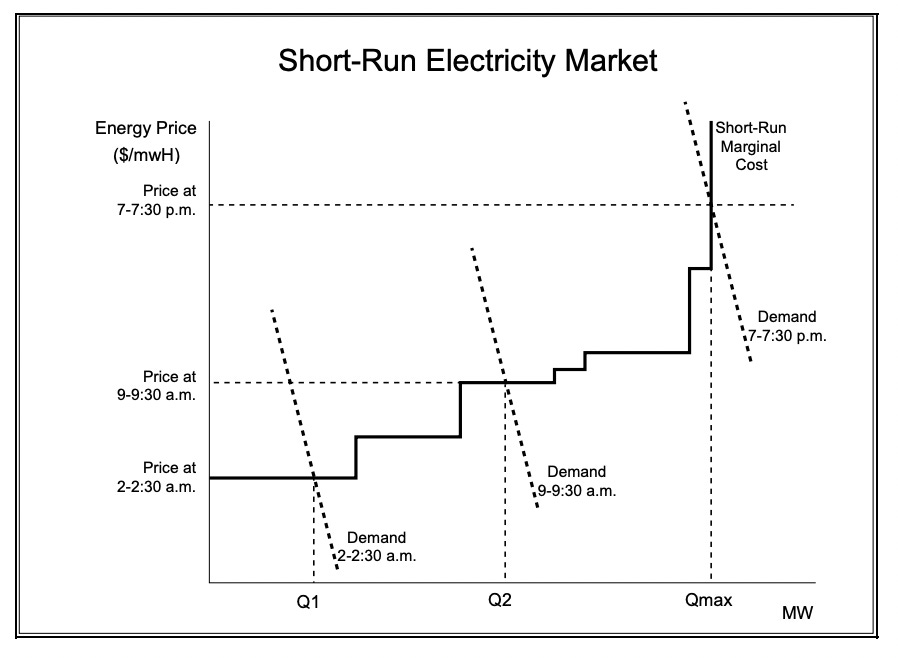

By the start of the 21st century, there was a competitive market for electric generation in most of the United States. Satisfying the policy diktat to maintain open and non-discriminatory access to the transmission system, and the engineering reality that an electric grid always needs to be balanced, led to the development of the concept of the independent system operator (ISO). ISOs schedule transmission and operate real-time and day-ahead markets for electricity. Wholesale power markets are essentially reverse auctions - generators specify the price they need to receive in order to supply a given amount of power.

Figs. 5-6: In restructured electricity markets, generator companies (“Gencos” in the diagram below) bid into a competitive auction. The bundled model, based on average cost, is replaced with a competitive model, in which generators sell their power at the market clearing price. This leads to two tricky problems - how to ensure peaking plants can recoup their costs, and how the introduction of zero-marginal cost resources (solar and wind) affects auction outcomes.

There are really four basic business models in restructured electricity markets. Generators produce power and sell it either at the market price or through bilateral PPAs. Transmission and distribution (“T&D”) utilities continue to be regulated monopolies, charging more-or-less uniform rates that reflect the cost of service, plus an allowed return on capital. In some states, marketing to end customers is also deregulated (“retail choice”). Finally, traders inject liquidity into the market and enable price discovery when they buy and sell wholesale power.

You can see each of these ideal types clearly when you plot US electricity market participants by the share of power sold to end customers (x-axis) and the percentage of power sales sourced from their own generation. Pure-play generators produce their own power, but mostly sell it to utilities, rather than end users; T&D utilities buy wholesale power and deliver it to customers. Traders, as intermediaries in the wholesale market, appear on the bottom left of the chart; and, finally, traditional, bundled utilities appear on the top right.

Fig. 7: Utilities can be mapped onto a 2x2 matrix, based on whether they generate their own power or buy it on the open market, and based on whether they sell power to end users, or to regulated, “lines and wires” utilities that handle delivery.

II. Different shades of green: benchmarking utility generation mix

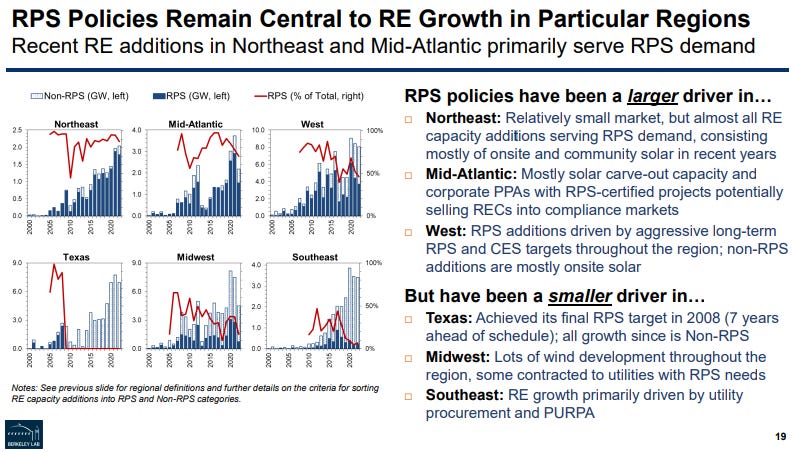

A key takeaway is that T&D utilities can only steer investment in generation indirectly (e.g. through lobbying). In the US, many states have instituted renewable portfolio standards (RPS), which require utilities to buy a certain share of their power from renewable sources. In practice, RPS targets have been more of a floor than a ceiling. Since 2000, renewable generation in the US has grown by more than twice the minimum required by state-level RPS, driven by voluntary demand from corporates with clean power targets, utilities, and retail green power options. However, RPS targets have been much more important in driving renewable deployment in the parts of the country that restructured their electricity markets (in the West, Mid-Atlantic, and Northeast).

I would hazard a guess that this is because the economics of building solar and wind in the Northeast are much worse than in, say, Texas or the Great Plains. Building renewables (like building anything else) costs more in the Northeast and California, and, in the Northeast, the “resource potential” for renewables is much lower (it is less windy and/or sunny).3 That combination means that the levelized costs of solar and wind power in the Northeast would not be competitive with fossil fuels, sans a regulatory requirement to buy it. Conversely, in Texas, even without an RPS in force, wind farms often generate more than half of the state’s power.

Figs. 8-10: RPS policies drive renewable deployment in the Northeast, where solar and wind face higher construction costs and lower capacity factors, which makes it hard for them to compete with fossil fuels. In other regions of the country that either lack RPS targets or, like Texas, surpassed them long ago, market-driven deployment of solar and wind is outpacing capacity additions in RPS states.

(Lawrence Berkeley National Laboratory)

My basic framework is that independent power producers (IPPs) and T&D utilities don’t have a lot of agency in shaping the US energy system. They simply build or buy (respectively) the power resources that make the most sense for them, based on a combination of regulation, input costs, and natural resource potential. One caveat is that credible, voluntary commitments to procure clean power by large commercial and industrial (“C&I”) customers and T&D utilities could promote investment in clean power, by providing developers with visibility into long-term demand for renewable PPAs.4 But the real action is clearly at bundled utilities, since they drive generation and transmission planning in their franchise territories.

Using EIA data, I compiled a list of the 50 largest utilities in the US that produce over 33 percent of the power they distribute to end users, along with the generators they own, and actual generation by fuel in 2022. I calculated emissions for each utility using the EIA’s published emissions factors for different fuels, and cross-checked the results with the Edison Electric Institute’s reporting database.5

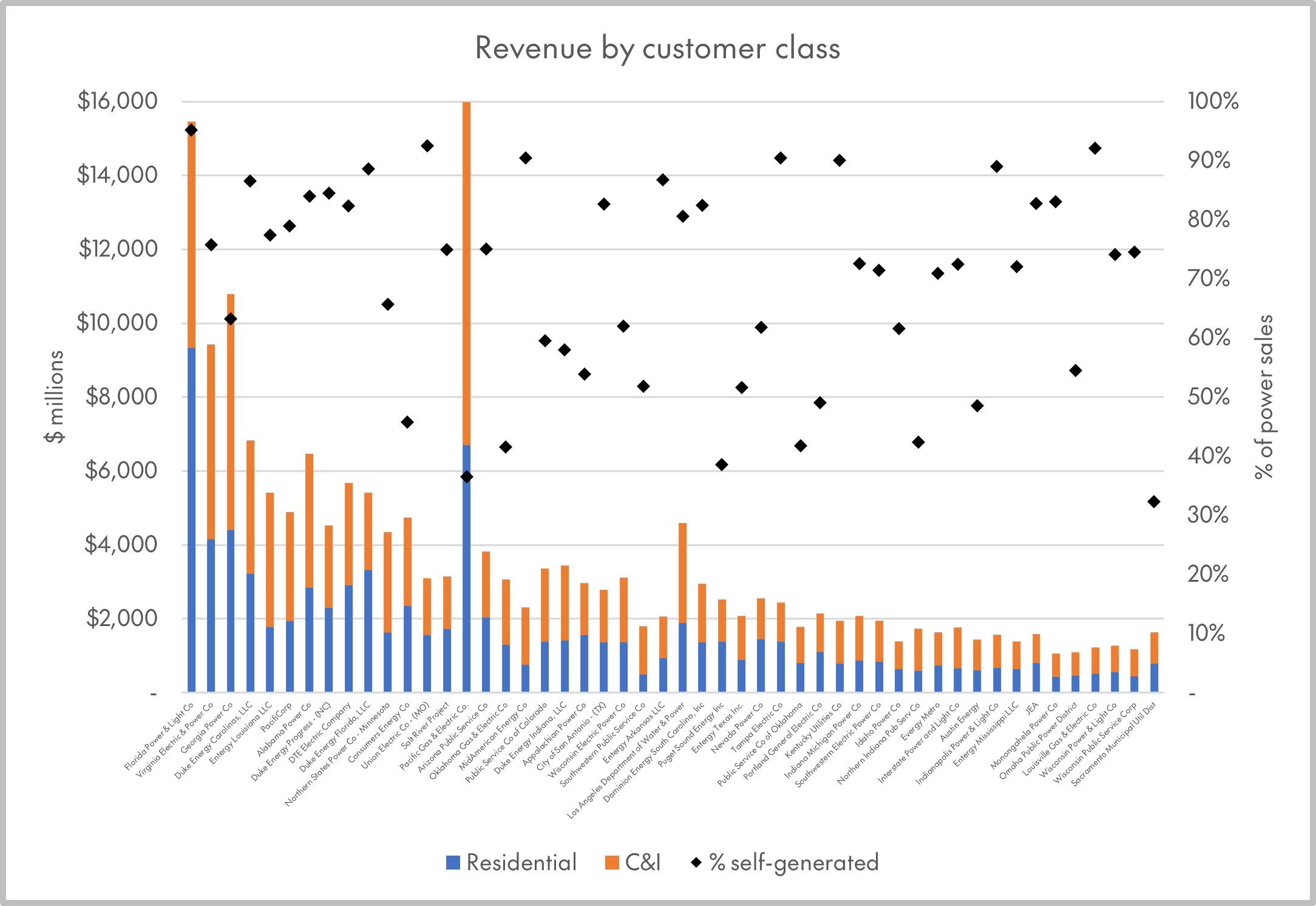

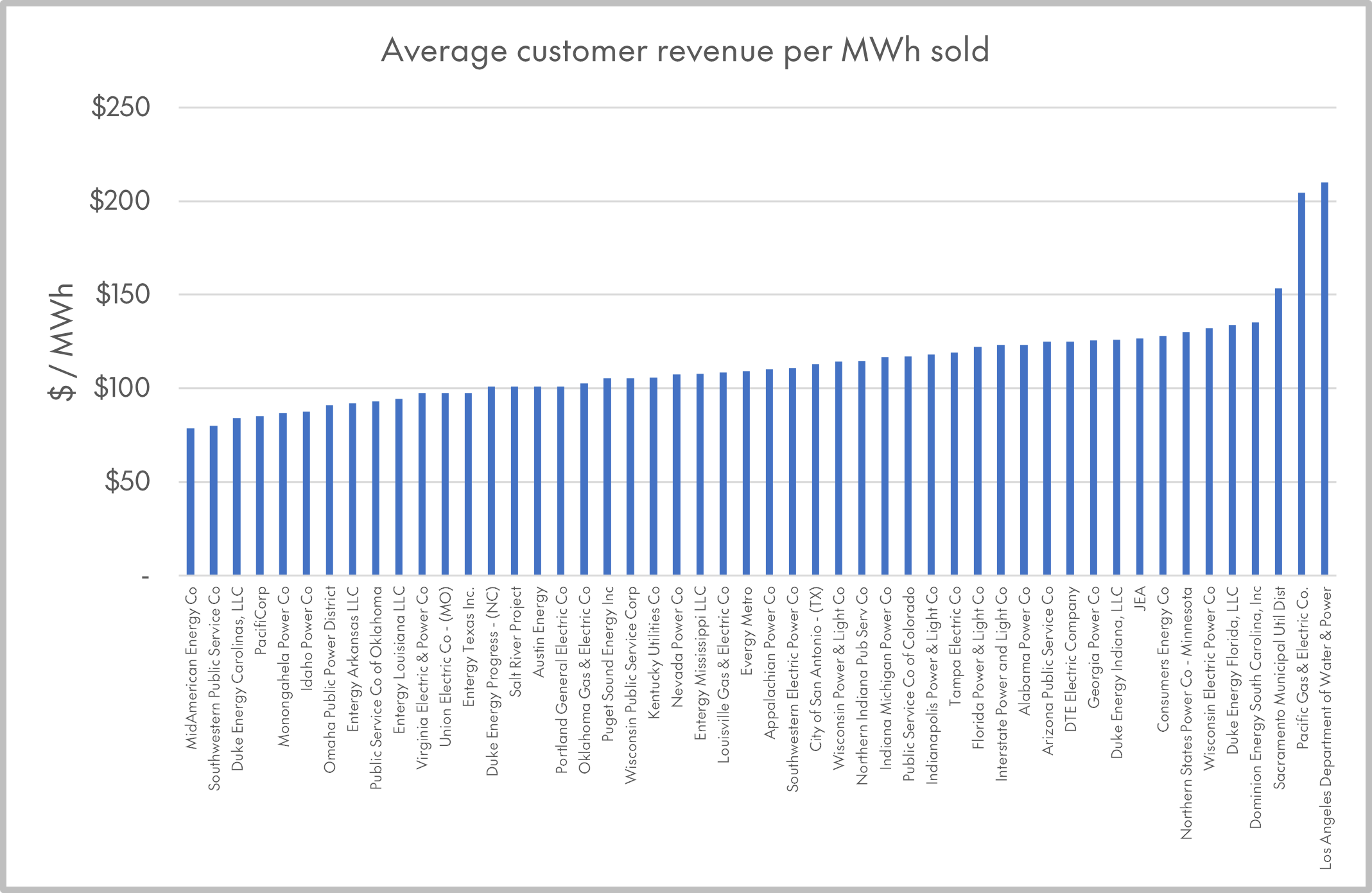

Figs. 11-12: Total revenue from customer sales split by residential or commercial and industrial (“C&I”) account for the 50 largest US utilities generating > 33% of the power they sold in 2022; below, average customer sales revenue per MWh sold.

(Energy Information Administration)

The really stark takeaway is just how different the biggest utilities’ generator stacks are. Utilities serving 6.1 million retail customers rely on fossil fuels for less than half of their total generation capacity. Utilities serving 10.6 million retail customers rely almost exclusively on fossil fuels (> 90%). And a far greater number of households, 37.2 million, get their power from a utility that’s somewhere in between.

Looking at actual generation, and at emissions intensity, illustrates a few nuances. One is the power of nuclear baseload generation for lowering the overall emissions intensity of the grid. On average, utilities that own nuclear generators are able to run them 86 percent of the time. That compares to 37 percent for coal and 30 percent for natural gas. While nuclear projects have struggled with rising construction costs for many decades, gigawatt for gigawatt, existing nuclear plants punch above their weight when it comes to avoiding fossil fuel emissions.

Another nuance is that there is a lot of variation in the emissions intensity of fossil generation - not just because gas is cleaner than coal (at least at the point of combustion - whether it is all that cleaner on a “lifecycle” basis is debatable), but because newer fossil generators typically operate at higher heat rates (thermal efficiency), which means they need to burn less fuel for each MWh of power they produce. Heat rates for gas-fueled plants varied from less than 30 percent (with Evergy Metro, the Kentucky Utilities Co., and the Omaha Public Power District as the worst offenders) all the way to 50 percent.

The result is that a utility’s emissions intensity is closely but far from perfectly correlated with the share of power produced by burning fossil fuels. That allows companies with generator fleets skewed toward newer combined-cycle gas plants (like NextEra) to burnish their green credentials, while kicking the can down the road on deeper decarbonization.

Figs. 13-14: Nameplate capacity and actual generation by fuel, based on 2022 data.

(Energy Information Administration)

Fig. 15: CO2 intensity of self-generated power as a function of the share of generation coming from fossil fuels.

(Energy Information Administration)

Parting thoughts

Shareholder activists clearly recognize the importance of utilities as grid planners. Between 2019 and 2024E, activists proposed an average of 8 climate-focused resolutions targeting US gas and electric utilities per year. As with other climate-related proposals, investor support for those resolutions that make it to a vote has been falling, from an average of 37 percent in calendar 2021 to 17 percent last year.

Making the case for more aggressive decarbonization targets in the utility sector basically means calling for bundled utilities to invest more in transmission, storage, and low-carbon generation. For that to happen, shareholders, lenders, regulators, workers, and customers need to align on a way of apportioning the costs and benefits of faster decarbonization that they can all live with. The investor perspective is particularly important, since investors will provide the capital to fund all this low-carbon investment.

In part 2, I’ll examine utilities as equity and fixed income investment vehicles, with NextEra and its regulated subsidiary, Florida Power & Light Co., as a case study. In part 3, I’ll connect the dots between utilities’ GHG targets and their path to future value creation.

With the Federal Power Commission, now the Federal Energy Regulatory Commission (FERC), regulating interstate transmission (~= the wholesale power market).

This section draws heavily on VanDoren (1998) and Lave et al. (2004).

To put some numbers around this, in 2021, the average solar plant in the Northeast cost $2,988 per kW to build, versus $1,431 per kW in the South (+109 percent), $1,445 per kW in the West (+107 percent), and $1,770 per kW in the Midwest (+69 percent). Likewise, wind generators cost $2,863 per kW to build in the Northeast, a 147 percent premium above construction costs in the South, 87 percent premium above costs in the West, and 83 percent premium above the Midwest.

State-level data is not available for wind, and shows that in California, the solar construction cost premium is not quite as severe compared to other states that added large amounts of solar capacity - solar installations cost 46 percent more than in Florida, and 20 percent more than in Texas, but were in line with North Carolina and Georgia. Looking across all generation technologies, average power plant construction costs were much higher in California than the other three states with the most capacity additions - Florida (+159 percent), Texas (+78 percent), and Ohio (+70 percent) - but I would take these numbers with a grain of salt, since capacity additions in FL, TX and OH included a higher share of gas plants, which cost less to build than renewables.

Once solar and wind plants are built, they generate power far less often in the Northeast than in the Southwest or even much of the Midwest. Solar capacity factors range from 18 to 20 percent in Maryland, New Jersey, Pennsylvania, New York, Connecticut, and Maine. In Vermont, Massachusetts, and Rhode Island, solar panels only generate power a dismal 16 to 17 percent of the time. This compares to capacity factors of 28 to 30 percent in Utah, Arizona, Nevada, and California, 23 to 26 percent in the Deep South, and 20 to 24 percent in much of the Midwest. Likewise, wind farms in the Great Plains can reach capacity factors of 40 to 50 percent, while capacity factors in the Northeast are more like 25 to 35 percent.

With construction costs ~2x lower-cost regions of the country, and capacity factors that are ~1/3 lower, the all-in, levelized cost of renewables in the Northeast is ~3x what they cost in the parts of the country that are best for building wind and solar.

For example, a solar developer can look at AWS, Azure, and GCP’s net zero goals, the IEA’s forecast that data center electricity demand will grow by 30 percent from 2022 to 2026, and make an informed guess that the price of solar and wind PPAs will continue to rise.

The EEI CO2 database isn’t 100 percent comparable with the numbers I present in this piece, since it includes a calculation for residual emissions intensity (i.e. emissions from power purchased in the wholesale market). Excluding one outlier, Monongahela Power, the data sets are very correlated (R-squared of 0.83). I present my calculations based on EIA data, rather than the self-reported EEI numbers, for greater comparability and because as outlined above, I put more weight on emissions from self-generated electricity.